Wood Mackenzie’s annual Renewables Briefing took place on 30 April 2024 in London. They are a consultancy that provides data, analytics, insight, and events around the energy transition.

Events like these are good opportunities to gain insights into the industry’s state, the participants’ moods, and what they expect in the future.

Below are some key takeaways from the event.

European Power Markets (presented by Dan Eager)

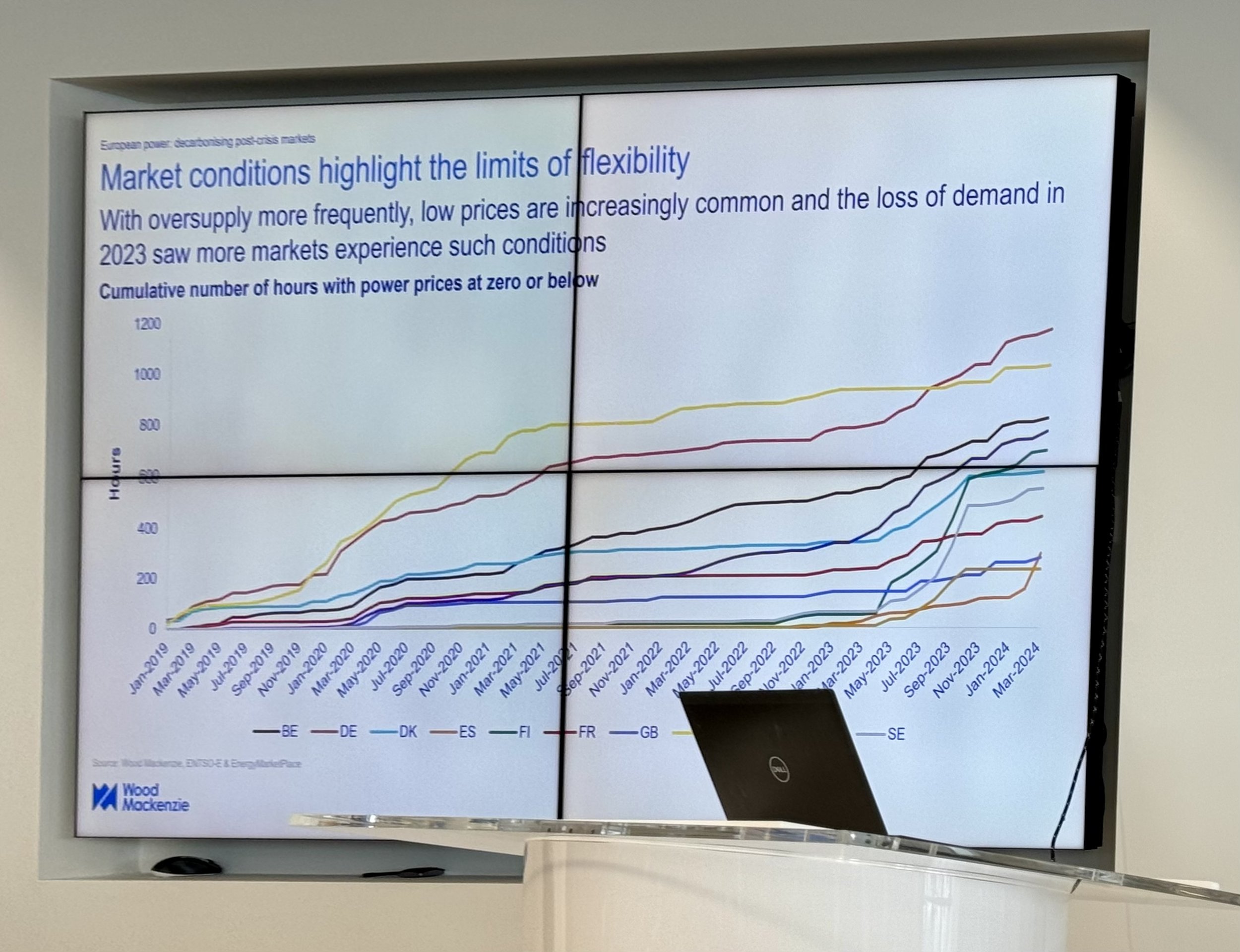

Electricity demand keeps falling due to improved efficiencies and demand destruction caused by the Ukraine war. At the same time, more intermittent electricity generators are being commissioned, replacing old coal, gas, and nuclear power plants.

This leads to an increasing number of times of „oversupply“ and hours with negative energy prices. The chart below shows the cumulative hours with negative pricing for several European countries.

Source: Wood Mackenzie

These negative prices open up new arbitrage trading possibilities for energy storage projects (charge the battery when the prices are negative and discharge it when the prices are high).

Wood Mackenzie forecasts that baseload electricity prices will stabilise in the range of €40/MWh (Nordics) to €60/MWh (Germany, Italy, UK) after 2030. However, the capture rates for solar and wind projects without energy storage will continue decreasing.

We have probably reached a turning point for corporate PPA prices, as several projects are no longer viable and will not be built. This will reduce supply and increase prices again.

Electricity demand in Germany will keep falling until 2030, before the full effect of electrification kicks in.

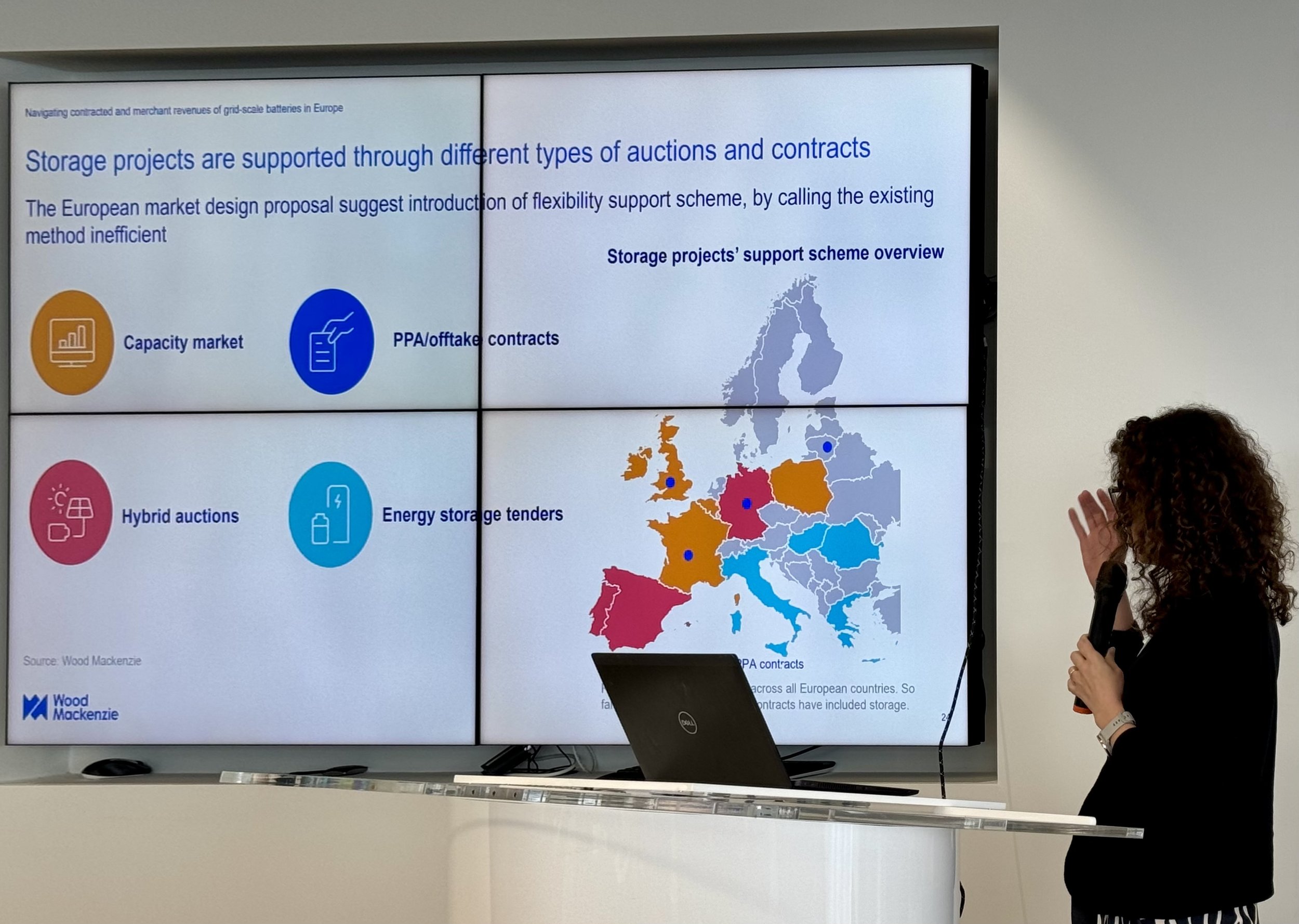

Energy Storage (presented by Anna Damani)

Governments and TSOs support the deployment of more energy storage as more and more intermittent generators are coming online. There is no unified support mechanism in Europe. The slide below shows the systems on a country-by-country basis.

Source: Wood Mackenzie

Wood Mackenzie forecasts the installed storage capacity (excluding pumped hydro) to grow from 9GW to 100GW by 2033, with the UK (20%), Italy (17%) and Germany (15%) becoming the most significant markets.

Ancillary markets are lucrative, but only for first movers and some countries, like the UK, already have an oversupply. This leaves energy trading and government tenders as the most important revenue component going forward.

Currently, the upper limit for economically viable lithium-ion batteries lies around 5 to 6 hours. Beyond that, we will need new technologies to achieve true long-term energy storage.

Long-duration energy storage capacity will only grow significantly from 2030 onwards and will need subsidies to be built.

My thoughts

The days of making money by building a pure wind or solar project are over. Too much intermittent generation is being built, and simply bolting some energy storage solution onto your generator is only a temporary fix. The big winners will be IPPs and strategic investors who hold large portfolios with multiple generation technologies and large energy storage capacities. They can offer (almost) baseload green power levels that are no longer tied to a single asset.