Introduction

The Watson Farley & Williams (WFW) spotlight series of events highlight one country at each event, and the panellists discuss the status of the renewable market in that country at a high level.

Germany was one of the first European markets to support renewable energy projects but still heavily depends on coal and lignite for power generation. Last year, the remaining nuclear plants were switched off, and the government is committed to phasing out coal and lignite by 2030 as part of the energy transition.

The government sees Natural gas as an important bridge fuel to guarantee baseload supply despite a push to increase the wind and solar PV capacity. As a result, several on-shore LNG terminals are being built right now to replace the Russian gas used previously.

Panelists

The panel is made up of the following:

Thomas Hollenhorst (Partner at WFW)

Dr Christine Bader (Partner at WFW with a focus on offshore wind)

Britta Katrin Wißmann (Partner with a focus on onshore wind)

Verena Scheibe (Partner with a focus on solar PV) unfortunately couldn’t attend.

Insights They Shared

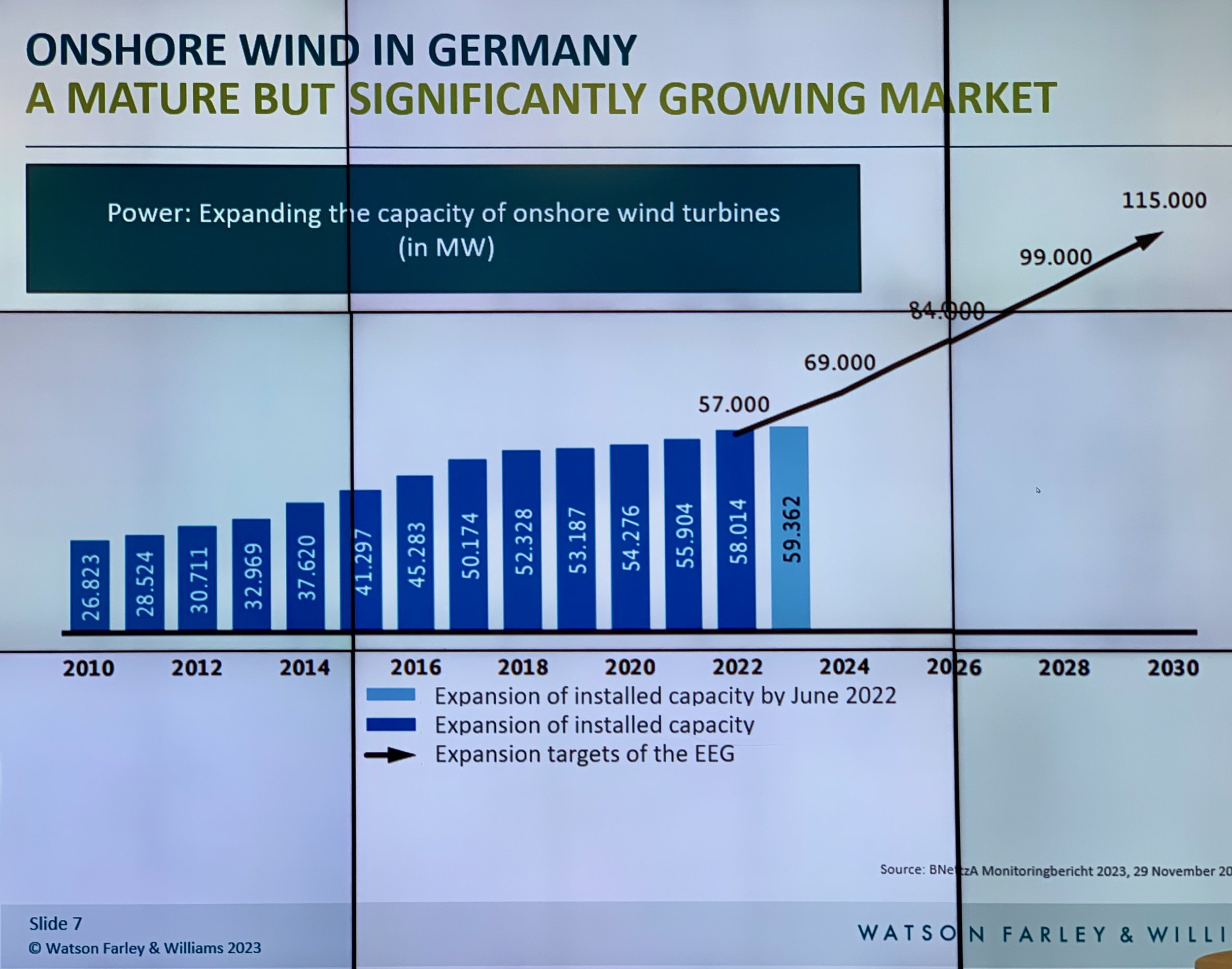

Onshore Wind

Legislation has set capacity targets, and 2% of federal land is set aside for new projects. However, the planning process makes the realisation of new projects difficult.

An increasing number of older projects reach the end of the 20-year subsidy period. These projects interest developers who want to repower them (replace the older smaller turbines with newer ones). Using fewer and more powerful turbines reduces operating costs and makes it easier to get a new permit whilst staying within the limit of the existing export connection.

New and repowered wind farms can bid for government subsidy contracts (EEG) in quarterly auctions.

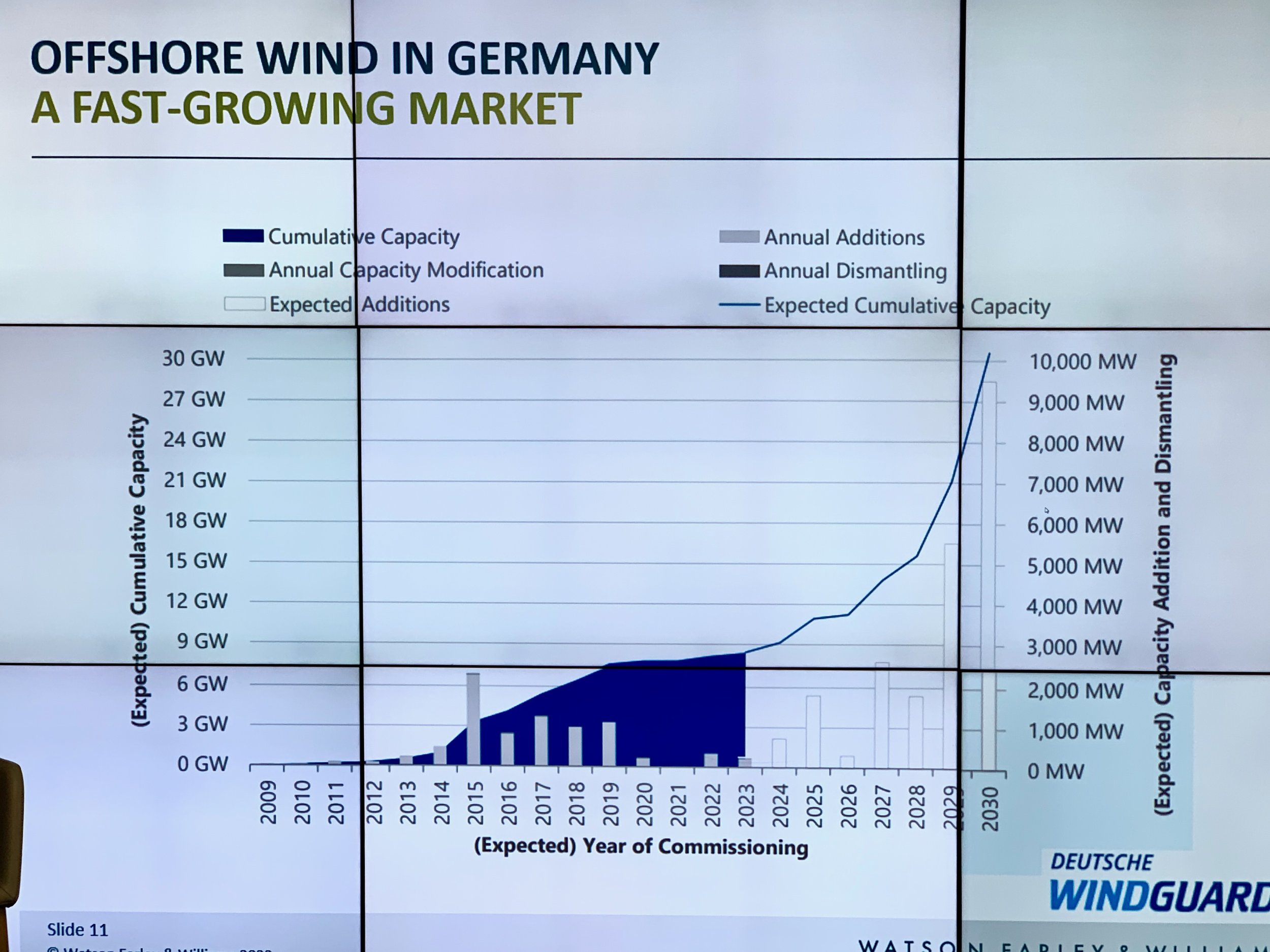

Offshore Wind

The offshore wind market is split into different types of auctions, one for projects that want government support through the EEG and one for subsidy-free projects.

Similar to the EEG system, projects need to compete in an auction process by bidding a price per Megawatt hour. Historically, most parties asked for very low support levels or even €0/MWh. But in last year’s auction, applicants (oil and gas majors) offered to pay the government for licenses for the first time.

The government has also set aside areas for subsidy-free projects with pre-determined capacities. Licences are granted based on such criteria as environmental impact or how many vocational training places are being created.

Solar PV

The German government plans to increase the installed capacity of solar PV from ca. 70 GW today to 250 GW by 2030. The goal is to split the increase 50/50 between ground-mounted solar and roof-top PV. Dedicated land has been set aside for new projects, and network operators must connect new plants.

The qualification criteria for the government support scheme EEG are stringent, and most projects don’t qualify. As a result, most asset owners choose to get PPAs instead.

The project finance market for <50MWp projects is dominated by smaller banks, and the KfW loan programme offers more favourable interest rates than most commercial banks can offer on their own.

While the renewable energy legislation allows for the installation of AgriPV plants, only a few pilot projects have been realised. The EEG support level is too low to cover the increased costs of AgriPV schemes compared to ground-mounted plants. A separate auction system for AgriPV is being considered as a result of this.

Green Hydrogen

The first projects are being developed, but there are still several uncertainties around how much demand there is, as the industrial sector has only started the transition.

An additional complication is EU directives, which state that renewable energy needs to come from newly installed capacity and that a direct agreement between the generator and the hydrogen producer needs to be in place.

Battery Storage

Germany is highly interconnected with its neighbours. For a long time, the government focused on the build-out of the transmission network. The battery storage sector is, therefore, still in its infancy.

Three types of projects are currently being built in Germany:

co-located batteries to sell power during the evening peak

large-scale batteries for the balancing market

transmission line connected batteries operated by the line owners

The revenue opportunities are somewhat limited as Germany doesn’t have a capacity market, and batteries can’t bid for frequency response services.

My Thoughts

Germany was one of the pioneers in Europe regarding subsidy schemes for renewable energy projects. But this is only half of the story, as the government looked at the same time to coal, lignite, and (Russian) natural gas to secure a stable baseload supply of electricity. The need to decarbonise and the war in Ukraine have upended this strategy.

Despite these changes, politicians haven’t really adjusted their thinking. They still push aggressively to expand renewable energy capacity while betting on natural gas and hydrogen to guarantee the supply of baseload.

The renewable energy market, especially wind and solar, is very attractive and attracts increasing foreign investments. In my opinion, the biggest risks are that many of the new gas and hydrogen projects become stranded assets when market demand fails to materialise.